Why was the August 2012 employment situation report so bad?

In a nutshell, it is because the companies that committed to participate in President Obama's latest ham-handed intervention in the economy, the 2012 Summer Jobs+ program, met their obligation and released their teen employees from their payrolls. The vast majority of the teens who were given summer jobs as part of the program have now gone back to school, and because they have done so, are no longer considered to be part the U.S. civilian labor force.

The removal of so many individuals from the ranks of the U.S. work force accounts for much of the reduction in the official U.S. unemployment rate from 8.3% to 8.1%.

Breaking down the August 2012 jobs numbers by age, we find that 204,000 teens are no longer being counted as being employed, while 250,000 fewer young adults between the ages of 20 and 24 are also being counted as having jobs.

Meanwhile, the number of individuals Age 25 or older counted as having jobs increased by 333,000. The resulting net change from July 2012 for the number of employed Americans was a loss of 119,000 jobs.

As of August 2012, there were 4,344,000 teens, 13,114,000 young adults and 124,643,000 adults Age 25 or older counted as being employed in the U.S. work force. The sudden disappearance of 202,000 jobs for teens represents a sudden decrease of four and a half percent in their numbers from the preceding month.

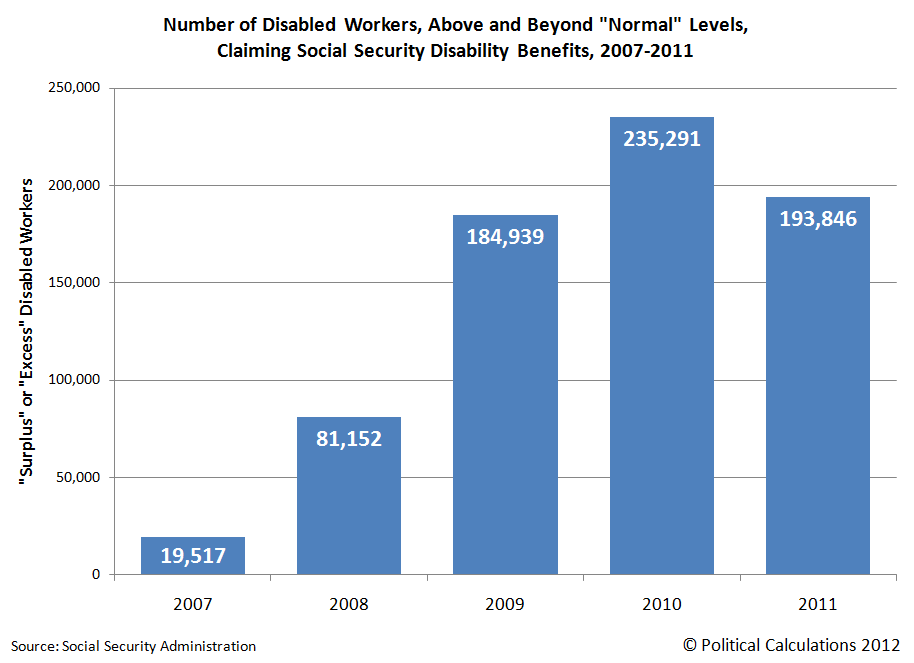

The following chart shows how that change affects both the unemployment rate for teens and what Age 16-19 unemployment rate would be if teens had the same labor force participation rate that they did in January 2009, when President Obama was sworn into office:

We've been tracking the influence of President Obama's 2012 Summer Jobs+ initiative upon the nation's jobs situation since the June 2012 jobs report came out, which showed an unexpected increase in the number of employed teens, seemingly at the expense of older members of the U.S. work force. That unusual pattern where teens, who lack the experience, education and skills that all older members of the U.S. work force have, suddenly seemed to be favored so much more by employers, continued in July 2012, even though the data clearly indicates that the program's hiring at its peak fell far short of stated expectations.

And now that the teen summer jobs program for 2012 has run its course, the employment data indicates that the "success" of the program was not sustained, with employment and labor force participation rate levels for U.S. teens immediately falling back to what they were before the program occurred. As far as the U.S. economy is concerned, it might as well never have happened.

Worse, it appears from the data that teens actually displaced older individuals from the U.S. job market while the program ran. The data for August 2012 suggests that the U.S. job market is going through somewhat of a correction, which we see in the sudden increase in the number of older individuals being counted as employed as compared to both June and July 2012, as they are no longer being directly displaced by the teens who gained employment as a result of the President's summer jobs program.

In a way, what we've just observed in the summer employment numbers for teens in the U.S. work force resembles President Obama's failed efforts to stimulate the auto industry with its "Cash for Clunkers" program in 2009 or to sustainably stimulate the housing market in 2010.

Like those economic policy failures, President Obama's latest economic initiative only succeeded in the equivalent of shifting around the deck chairs of the Titanic, imposing unnecessary additional costs on the U.S. economy at a time when it can not afford them. As a result, we must find that President Obama's economic policies are hurting the American people more than they are helping them.